Quick Answer

If you pay quarterly estimated taxes late, the IRS may charge an underpayment penalty based on the amount you should have paid, when it was due, and how long it stayed unpaid. Paying late is still usually better than waiting until you file, but it may not erase the penalty for the period you were short.

Key Takeaways

- Paying quarterly taxes late can create an underpayment penalty based on how much was underpaid and how long the shortfall remained unpaid.

- You can still pay after the due date. In fact, paying late is usually better than waiting until tax filing time.

- Catching up later can reduce the damage, but it usually doesn’t erase the penalty for the period you were underpaid.

- If you’re already behind and tax debt has built up, the fix is to separate old debt from current-year taxes, pay what you can, and get a realistic payment system in place.

Missing a quarterly estimated tax payment usually doesn’t cause an immediate crisis. That’s part of the problem.

You may not get a notice right away, and your bank account won’t freeze because you missed one estimate. But the IRS still tracks when tax should have been paid. If you were supposed to make quarterly estimated payments and didn’t, the shortfall can turn into penalties, interest, tax debt, and eventually collection pressure.

So when someone asks me, “What happens if I pay my quarterly taxes late?” I would say: it depends on how late, how much you owe, whether you’re current now, and whether this is a one-time miss or part of a bigger pattern.

What happens if I pay my quarterly taxes late?

If you miss a quarterly estimated tax payment, the IRS treats it as an underpayment. That means you may owe an added charge for paying late, plus interest that keeps building until the amount is paid.

Nobody is kicking down your door over one missed estimate. But the IRS meter does start running.

Federal income tax is pay-as-you-go. Employees usually cover it through withholding. But self-employment income, investment income, rental income, retirement income, and partnership or S corporation passthrough income may require individual quarterly estimated payments. Corporate estimates and payroll tax deposits follow separate rules.

Can I pay extra to catch up on missed quarterly payments?

Say you should have made a $4,000 estimated payment in April, but paid it in September. That payment reduces what you owe overall, but it does not make the April payment on time. The IRS can still charge you for the April-to-September underpayment period.

That’s why “I paid it eventually” does not always mean “I avoided the penalty.”

The penalty works more like interest than a standard late fee. The IRS looks at how much should have been paid, how much was actually paid, and how long the shortfall stayed unpaid. Each estimated tax period is measured separately, and the rate can change quarterly because it is tied to federal interest rates.

You could let the IRS calculate the penalty for you after you’ve filed. But if your income was uneven, or most of it came late in the year, Form 2210 may matter because timing can change the penalty calculation.

What if I haven’t been making estimated payments and now I owe tax debt?

If missed estimated taxes have turned into tax debt, here are a few practical steps to follow:

1) Find the real balance.

Gather IRS notices, state notices, prior-year tax returns, proof of estimated payments, current-year bookkeeping or a profit and loss report, W-2 withholding records, and any payment plan paperwork you already have.

You need to know:

- Which tax years have balances

- Whether each balance is federal, state, or both

- How much is original tax versus penalty and interest

- Whether estimated payments were credited to the right tax year

- Whether this year’s estimated payments are already falling short

If you put every available dollar toward last year’s balance but don’t cover this year’s estimated taxes, you may end up with a new tax bill when you file the next return.

2) File any missing returns.

If required returns are missing, get them filed before you try to set up payment terms. The IRS generally wants Sacramento taxpayers in filing compliance before it approves an installment agreement or offer in compromise.

Unfiled returns also make the numbers unreliable. The IRS may be working from notices, estimated balances, or incomplete information. Once the returns are filed, you can see the actual balance and decide whether to pay, request a payment plan, or look at another resolution option.

3) Estimate the current-year tax.

Before choosing a payment strategy, compare what has already been paid for this year against what the year is likely to owe. Look at:

- Current-year profit or income

- Federal tax already paid through withholding or estimates

- Self-employment tax, if applicable

- State estimated tax needs

- Expected income for the rest of the year

If every available dollar goes toward an old balance while this year’s estimates stay short, your next filed return may create a new balance. That can make getting approved for an installment agreement or keeping one you are already set up on more difficult.

4) Pay what you reasonably can now.

If you can pay the full balance, pay it.

If you can’t, make a realistic payment based on the full picture. That may mean paying toward the current-year shortfall first so you don’t create a new balance. Or it may mean paying an assessed balance that is already generating IRS notices.

But don’t drain your operating account so aggressively that your West Sacramento rent, payroll, groceries, or basic operating costs fail next month. That just creates another emergency.

Partial progress counts.

5) Set up a payment plan if the filed balance cannot be paid.

A short-term plan may work if you can pay the balance within a relatively brief period. A longer installment agreement may work if you need monthly payments.

A payment plan does not make penalties and interest disappear. But it can move the problem from “open-ended mess” to “monthly obligation.” That only works if you also stay current going forward. The IRS problem doesn’t really stabilize until the current year stops bleeding.

How can I avoid the penalty next time?

The best way to avoid future estimated tax penalties is to stop treating taxes as leftover money. Build them into your cash flow by estimating during the year, setting money aside as income comes in, and adjusting when income changes.

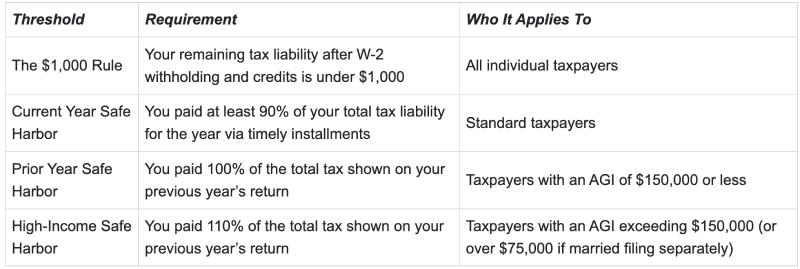

For many Sacramento taxpayers, one of these safe harbor rules is the starting point:

Advisor note: Safe harbor can help you avoid an estimated tax penalty, but it does not guarantee you won’t owe when you file. If income is up this year, last year’s number may not be enough.

Before each quarterly deadline, compare year-to-date profit, withholding, estimated payments already made, and expected income for the rest of the year. If your income is uneven, ask about the Annualized Income Installment Method on Schedule AI of Form 2210.

Final thoughts

Missed estimated taxes are fixable, but you need a real plan.

If quarterly taxes have gotten away from you, don’t wait for the next notice to force the issue. Let’s get the numbers out in the open and build a plan that fits your situation.

You know where to find us: sacramentotaxresolution.com/schedule-an-appointment/

FAQs

“What happens if I pay my quarterly taxes late?”

If you pay quarterly estimated taxes late, the IRS treats the missed amount as an underpayment. You may owe an estimated tax penalty based on the amount underpaid and how long it stayed unpaid, even if you catch up before filing your return. Paying as soon as possible can reduce the amount that keeps building.

“Can the IRS waive my estimated tax penalty?”

Yes, but the IRS only waives estimated tax penalties in specific situations. You request the waiver on Form 2210 and explain why the penalty should be removed or reduced. Relief may apply after a casualty, disaster, or other unusual circumstance. It may also apply in some retirement or disability situations when the underpayment was due to reasonable cause and not willful neglect.

“Can I use my tax refund to cover missed estimated taxes?”

You can elect to apply a tax overpayment to the following year’s estimated taxes, which the IRS treats as a timely payment made on the first quarter’s due date. However, you cannot use a year-end refund to retroactively erase an underpayment penalty that accrued during earlier quarters of that same tax year. Because estimated tax penalties are calculated on a period-by-period basis, a later credit will only stop the penalty from growing, not wipe out past months of underpayment.

“Are estimated tax penalties deductible?”

No, estimated tax penalties are not deductible on either your personal or business tax returns. The IRS treats these penalties as an addition to your underlying tax liability rather than a legitimate cost of doing business, meaning they cannot be used to reduce your taxable income.

“What records should I keep after making estimated tax payments?”

You should maintain a clear paper trail by saving digital confirmation receipts from IRS Direct Pay or the EFTPS system, alongside bank statements showing the funds being debited. If you still pay by mail, retain physical copies of the canceled checks and their matching Form 1040-ES vouchers to ensure you receive proper credit at tax time. It is best practice to track these payment dates and exact amounts in a dedicated spreadsheet and keep all supporting documentation for three to seven years.

“Can withholding fix a missed estimated tax problem?”

Yes. Increasing withholding later in the year can sometimes reduce or even eliminate an estimated tax shortfall. Federal withholding is generally treated as paid evenly throughout the year, which can make it more flexible than a late estimated payment. This may work if you, your spouse, or your S corporation can still adjust W-2 wages and there are enough paychecks left to make the change matter.